Top 14 Neobanks in India & Best Digital Banking Apps

Digital banking is evolving quickly, and neobanks are leading that shift by offering app-first financial services without traditional branches. From smart savings accounts to flexible credit and business banking tools, these platforms are changing how people manage money. In this blog, we will take a look at the top 15 neobanks in India and what makes each one worth considering.

What are Neobanks?

A neobank is a "digital-only" bank that exists entirely on your smartphone or computer. Unlike traditional banks, neobanks have no physical branches. They use advanced technology to offer faster, cheaper, and more user-friendly financial services, such as instant account opening, real-time spending alerts, and no-fee checking.

Why are they called "Neo" banks?

The word "Neo" comes from the Greek word for "new." They represent a new era of banking designed for the internet age, focusing on transparency, speed, and automation rather than paperwork and long lines.

Top 14 Neobanks in India

| Sr. No. | Neobank | Key Services | Interest / Returns | Best For |

|---|---|---|---|---|

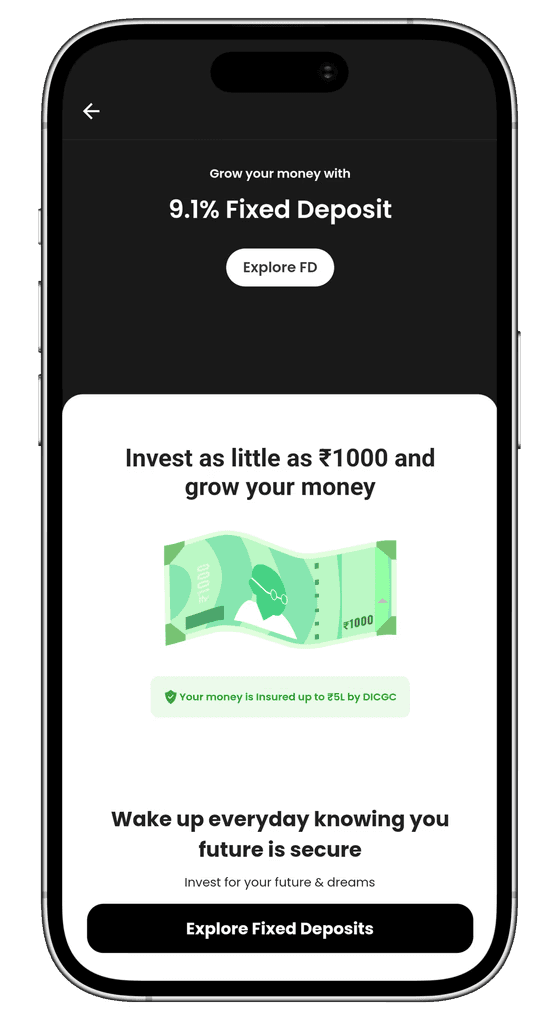

| 1 | Freo | Neobank offering savings, flexible credit line, cards, and BNPL in one app. | Savings interest follows partner bank rates. 9.1% return on fixed deposit. | Millennials and professionals wanting banking plus flexible credit. |

| 2 | Fi Money | Digital savings and salary account with rewards, UPI, and saving jars via Federal Bank. | Savings interest typically around 2.5–3% p.a., depending on balance slabs. | Salaried users who want a modern rewards-based banking app. |

| 3 | Jupiter | App-first savings account with budgeting tools, spending insights, and auto-saving pots. | Savings rates aligned with Federal Bank’s slab-based rates in the low single digits. | Users who want strong spending analytics and a simple banking app. |

| 4 | Niyo | Travel-focused digital banking with international card and forex-friendly features. | Certain savings variants offer higher interest, up to roughly 7% on some balance slabs. | Travellers and students spending internationally. |

| 5 | RazorpayX | Business neobank with current accounts, automated payouts, and tax/payment integrations. | Current accounts are transaction-focused, with minimal interest depending on bank terms. | Startups and digital businesses managing finance operations. |

| 6 | InstantPay | Digital current accounts with collections, payouts, and SME banking tools. | Returns depend on partner banks and are not the main focus of the platform. | Small and mid-sized businesses wanting simple branchless banking. |

| 7 | FamPay | Teen payment app with parental controls and numberless card for minors. | Works as a prepaid spending tool rather than an interest-earning account. | Families introducing teens to digital payments safely. |

| 8 | Mahila Money | Financial platform offering savings access, loans, and insurance for women through partners. | Interest depends on partner institutions providing the savings products. | Women entrepreneurs and first-time borrowers. |

| 9 | Open Money | SME neobank with current accounts, invoicing, expense management, and business credit. | Business accounts usually do not focus on high interest; returns follow bank policies. | SMEs needing banking, payments, and finance tools together. |

| 10 | Stashfin | Digital line-of-credit card with flexible borrowing and rewards. | Interest applies to borrowed credit similar to credit cards or personal loans. | Users needing quick and flexible credit access. |

| 11 | Chqbook | Multilingual digital current account for small merchants and shop owners. | Interest follows partner bank policies and is not a primary feature. | Kirana stores and small local businesses. |

| 12 | ZikZuk | SME finance platform with founders’ credit card and cash-flow dashboards. | Interest comes from linked bank accounts rather than the platform itself. | Business owners wanting better financial visibility. |

| 13 | Finin | Early consumer neobank focused on goal-based saving, now part of Open. | Savings rates earlier followed partner bank policies. | Example of early neobank UX in India. |

| 14 | Zolve | Cross-border neobank helping Indians open US bank accounts and credit before relocation. | Offers competitive APY through US partner banks, varying over time. | Indian students and professionals moving abroad. |

| Sr. No. | Neobank | Key Services | Interest / Returns | Best For |

|---|---|---|---|---|

| 1 | Freo | Neobank offering savings, flexible credit line, cards, and BNPL in one app. | Savings interest follows partner bank rates. 9.1% return on fixed deposit. | Millennials and professionals wanting banking plus flexible credit. |

| 2 | Fi Money | Digital savings and salary account with rewards, UPI, and saving jars via Federal Bank. | Savings interest typically around 2.5–3% p.a., depending on balance slabs. | Salaried users who want a modern rewards-based banking app. |

| 3 | Jupiter | App-first savings account with budgeting tools, spending insights, and auto-saving pots. | Savings rates aligned with Federal Bank’s slab-based rates in the low single digits. | Users who want strong spending analytics and a simple banking app. |

| 4 | Niyo | Travel-focused digital banking with international card and forex-friendly features. | Certain savings variants offer higher interest, up to roughly 7% on some balance slabs. | Travellers and students spending internationally. |

| 5 | RazorpayX | Business neobank with current accounts, automated payouts, and tax/payment integrations. | Current accounts are transaction-focused, with minimal interest depending on bank terms. | Startups and digital businesses managing finance operations. |

| 6 | InstantPay | Digital current accounts with collections, payouts, and SME banking tools. | Returns depend on partner banks and are not the main focus of the platform. | Small and mid-sized businesses wanting simple branchless banking. |

| 7 | FamPay | Teen payment app with parental controls and numberless card for minors. | Works as a prepaid spending tool rather than an interest-earning account. | Families introducing teens to digital payments safely. |

| 8 | Mahila Money | Financial platform offering savings access, loans, and insurance for women through partners. | Interest depends on partner institutions providing the savings products. | Women entrepreneurs and first-time borrowers. |

| 9 | Open Money | SME neobank with current accounts, invoicing, expense management, and business credit. | Business accounts usually do not focus on high interest; returns follow bank policies. | SMEs needing banking, payments, and finance tools together. |

| 10 | Stashfin | Digital line-of-credit card with flexible borrowing and rewards. | Interest applies to borrowed credit similar to credit cards or personal loans. | Users needing quick and flexible credit access. |

| 11 | Chqbook | Multilingual digital current account for small merchants and shop owners. | Interest follows partner bank policies and is not a primary feature. | Kirana stores and small local businesses. |

| 12 | ZikZuk | SME finance platform with founders’ credit card and cash-flow dashboards. | Interest comes from linked bank accounts rather than the platform itself. | Business owners wanting better financial visibility. |

| 13 | Finin | Early consumer neobank focused on goal-based saving, now part of Open. | Savings rates earlier followed partner bank policies. | Example of early neobank UX in India. |

| 14 | Zolve | Cross-border neobank helping Indians open US bank accounts and credit before relocation. | Offers competitive APY through US partner banks, varying over time. | Indian students and professionals moving abroad. |

Which is The Best Neobank in India?

1

Freo

Freo stands out as one of the most well-rounded neobanking apps in India because it combines saving, credit, and everyday money management in one place. Instead of using separate apps for borrowing, tracking expenses, and managing payments, you get a more connected experience here.

Best for:

Users who want savings and flexible credit in one app

Salaried millennials and young professionals

People looking for a practical alternative to traditional banking apps

Key features:

Digital savings and deposit products through partner banks

Personal credit line, cards, EMI options, and BNPL access

Expense tracking and money management tools

Fixed deposits with an impressive 9.1% return rate.

Why choose it:

Freo works well if you want one app that supports both daily spending and credit needs without feeling scattered.

2

Fi Money

Fi Money is a polished consumer neobank that offers a zero-balance digital savings and salary account through Federal Bank. Its clean app, rewards, and goal-based saving tools make it appealing to users who want banking to feel modern and easy to use.

Best for:

Salaried professionals

Users who like cashback and rewards

People who want a zero-balance digital account with UPI

Key features:

Zero-balance savings and salary account

Fi Jars for goal-based saving

Cashback, rewards, and app-based controls

Why choose it:

Fi is a strong option if you want a salary account with useful saving tools, spending insights, and a more engaging app experience.

3

Jupiter

Jupiter is popular for keeping digital banking simple. It offers a zero-balance savings account with Federal Bank and focuses on clean design, smooth onboarding, and helpful budgeting tools for everyday users.

Best for:

First-time neobank users

Young professionals who want spending insights

Users looking for a simple zero-balance account

Key features:

Zero-balance savings account

Instant onboarding with UPI access

Budgeting, expense tracking, and saving pots

Why choose it:

Jupiter is a good fit if you want a clean, no-fuss app that helps you understand spending and manage savings better.

4

Niyo

Niyo is best known for travel-focused banking. It offers accounts and cards through partner banks and is especially useful for people who spend abroad and want to avoid high forex charges.

Best for:

Frequent international travellers

Students going abroad

Users who want lower forex costs

Key features:

Zero forex markup on select transactions

Travel-friendly account and card options

App controls for card use and tracking

Why choose it:

If overseas spending is a big part of your life, Niyo can help you save on forex fees and manage travel spending more smoothly.

5

RazorpayX

RazorpayX is built for startups and SMEs, not retail users. It helps businesses manage current accounts, payouts, payroll, taxes, and collections through one connected finance platform.

Best for:

Startups and digital businesses

Finance teams handling payouts and taxes

Businesses already using Razorpay services

Key features:

Digital current accounts

Automated payouts and collections

Tax payments and integrations with tools like Tally and Zoho

Why choose it:

RazorpayX is ideal if your business wants faster finance operations and less manual work across banking and payments.

6

InstantPay

InstantPay is a business-focused neobank designed for SMEs that want quick digital onboarding and easy access to current account and cash-management tools without traditional banking friction.

Best for:

Small and medium businesses

Firms with mobile-first teams

Businesses seeking simple digital current accounts

Key features:

Digital current accounts and cash-management tools

Collections, payouts, and reconciliation

Mobile and web access with multi-bank support

Why choose it:

InstantPay makes sense for businesses that want practical digital banking tools without moving into a more complex enterprise system.

7

FamPay

FamPay targets teenagers and families by offering supervised digital payments. It helps teens use UPI and cards while parents stay involved through funding and controls.

Best for:

Parents introducing kids to digital money

Teenagers making online and offline payments

Families building financial literacy early

Key features:

Teen-focused accounts with parental controls

Numberless card for added safety

UPI payments and spend tracking

Why choose it:

FamPay balances independence and supervision well, making it one of the more established options in India’s teen neobank segment.

8

Mahila Money

Mahila Money focuses on women, especially women entrepreneurs and first-time borrowers. Rather than offering generic fintech products, it tries to address real financial gaps faced by women-led businesses.

Best for:

Women micro-entrepreneurs

Home-based business owners

First-time women borrowers

Key features:

Savings, loans, and insurance through partners

Digital onboarding tailored to women-led ventures

Financial guidance and educational content

Why choose it:

Mahila Money stands out because it is built around financial inclusion and offers a more focused experience than mainstream banking apps.

9

Open Money

Open Money is one of the biggest SME neobanking platforms in India. It combines current accounts, invoicing, payouts, expense management, and business credit in one system.

Best for:

SMEs and startups

Founders who want more than a basic current account

Businesses looking for banking and invoicing together

Key features:

Business current accounts and expense tools

Integrated invoicing and payments

Credit access through partnerships

Why choose it:

Open is a great choice for business owners who want better control over everyday money movement instead of juggling separate tools.

10

Stashfin

Stashfin is more credit-focused than banking-focused. It offers a digital line-of-credit card with flexible access to funds, digital approval, and repayment options that appeal to users needing quick credit.

Best for:

Users with flexible credit needs

People who prefer revolving credit

Users looking to build or rebuild credit

Key features:

Digital line-of-credit card

Quick approval and disbursal

Cashback, ATM withdrawals, and EMI options

Why choose it:

Stashfin is useful if your main priority is flexible borrowing rather than a full-service banking setup.

11

Chqbook

Chqbook is built for small Indian business owners like kirana stores, local merchants, and proprietors. Its multilingual and mobile-first approach makes it more accessible for regional users.

Best for:

Kirana stores and local merchants

Small proprietors and neighbourhood businesses

Users who prefer vernacular interfaces

Key features:

Zero-balance digital current account

Multilingual app support

Basic banking tools plus access to loans and insurance

Why choose it:

Chqbook feels more rooted in the needs of small Indian businesses than many startup-focused fintech platforms.

12

ZikZuk

ZikZuk, from the Zaggle group, focuses on financial visibility for SMEs. It combines a business credit card with dashboards that help founders track receivables, payables, and cash flow.

Best for:

SME founders with multiple accounts

Businesses wanting better cash-flow visibility

Founders who need a credit card plus finance dashboard

Key features:

Business credit card for founders

Finance dashboards and forecasting tools

Multi-bank account aggregation

Why choose it:

ZikZuk is useful if your main challenge is not just banking, but getting a clearer picture of your business finances in one place.

13

Finin

Finin was one of the early consumer neobanks in India and helped popularize app-first saving and goal-based money management. It has since become part of Open Financial Technologies.

Best for:

Users looking for easy onboarding and high security

People who need AI Powered Insights for their money

Key features:

Goal-based saving experience

Consumer-friendly digital banking design

Now supports Open’s broader banking infrastructure

Why choose it:

Choose it for its rapid, paperless onboarding, high-interest savings via partner SBM Bank, and smart spending analytics to achieve financial independence.

14

Zolve

Zolve focuses on Indians moving to the US or Canada. It helps students and professionals set up accounts and begin building credit before they arrive abroad.

Best for:

Indian students moving abroad

Professionals relocating to the US or Canada

Users who want banking ready before landing

Key features:

Cross-border account setup support

Credit cards without prior local credit history

Online application using Indian passport and visa details

Why choose it:

Zolve solves a real relocation problem by helping users start banking and credit-building early, which makes settling abroad much easier.

1

Freo

Freo stands out as one of the most well-rounded neobanking apps in India because it combines saving, credit, and everyday money management in one place. Instead of using separate apps for borrowing, tracking expenses, and managing payments, you get a more connected experience here.

Best for:

Users who want savings and flexible credit in one app

Salaried millennials and young professionals

People looking for a practical alternative to traditional banking apps

Key features:

Digital savings and deposit products through partner banks

Personal credit line, cards, EMI options, and BNPL access

Expense tracking and money management tools

Fixed deposits with an impressive 9.1% return rate.

Why choose it:

Freo works well if you want one app that supports both daily spending and credit needs without feeling scattered.

2

Fi Money

Fi Money is a polished consumer neobank that offers a zero-balance digital savings and salary account through Federal Bank. Its clean app, rewards, and goal-based saving tools make it appealing to users who want banking to feel modern and easy to use.

Best for:

Salaried professionals

Users who like cashback and rewards

People who want a zero-balance digital account with UPI

Key features:

Zero-balance savings and salary account

Fi Jars for goal-based saving

Cashback, rewards, and app-based controls

Why choose it:

Fi is a strong option if you want a salary account with useful saving tools, spending insights, and a more engaging app experience.

3

Jupiter

Jupiter is popular for keeping digital banking simple. It offers a zero-balance savings account with Federal Bank and focuses on clean design, smooth onboarding, and helpful budgeting tools for everyday users.

Best for:

First-time neobank users

Young professionals who want spending insights

Users looking for a simple zero-balance account

Key features:

Zero-balance savings account

Instant onboarding with UPI access

Budgeting, expense tracking, and saving pots

Why choose it:

Jupiter is a good fit if you want a clean, no-fuss app that helps you understand spending and manage savings better.

4

Niyo

Niyo is best known for travel-focused banking. It offers accounts and cards through partner banks and is especially useful for people who spend abroad and want to avoid high forex charges.

Best for:

Frequent international travellers

Students going abroad

Users who want lower forex costs

Key features:

Zero forex markup on select transactions

Travel-friendly account and card options

App controls for card use and tracking

Why choose it:

If overseas spending is a big part of your life, Niyo can help you save on forex fees and manage travel spending more smoothly.

5

RazorpayX

RazorpayX is built for startups and SMEs, not retail users. It helps businesses manage current accounts, payouts, payroll, taxes, and collections through one connected finance platform.

Best for:

Startups and digital businesses

Finance teams handling payouts and taxes

Businesses already using Razorpay services

Key features:

Digital current accounts

Automated payouts and collections

Tax payments and integrations with tools like Tally and Zoho

Why choose it:

RazorpayX is ideal if your business wants faster finance operations and less manual work across banking and payments.

6

InstantPay

InstantPay is a business-focused neobank designed for SMEs that want quick digital onboarding and easy access to current account and cash-management tools without traditional banking friction.

Best for:

Small and medium businesses

Firms with mobile-first teams

Businesses seeking simple digital current accounts

Key features:

Digital current accounts and cash-management tools

Collections, payouts, and reconciliation

Mobile and web access with multi-bank support

Why choose it:

InstantPay makes sense for businesses that want practical digital banking tools without moving into a more complex enterprise system.

7

FamPay

FamPay targets teenagers and families by offering supervised digital payments. It helps teens use UPI and cards while parents stay involved through funding and controls.

Best for:

Parents introducing kids to digital money

Teenagers making online and offline payments

Families building financial literacy early

Key features:

Teen-focused accounts with parental controls

Numberless card for added safety

UPI payments and spend tracking

Why choose it:

FamPay balances independence and supervision well, making it one of the more established options in India’s teen neobank segment.

8

Mahila Money

Mahila Money focuses on women, especially women entrepreneurs and first-time borrowers. Rather than offering generic fintech products, it tries to address real financial gaps faced by women-led businesses.

Best for:

Women micro-entrepreneurs

Home-based business owners

First-time women borrowers

Key features:

Savings, loans, and insurance through partners

Digital onboarding tailored to women-led ventures

Financial guidance and educational content

Why choose it:

Mahila Money stands out because it is built around financial inclusion and offers a more focused experience than mainstream banking apps.

9

Open Money

Open Money is one of the biggest SME neobanking platforms in India. It combines current accounts, invoicing, payouts, expense management, and business credit in one system.

Best for:

SMEs and startups

Founders who want more than a basic current account

Businesses looking for banking and invoicing together

Key features:

Business current accounts and expense tools

Integrated invoicing and payments

Credit access through partnerships

Why choose it:

Open is a great choice for business owners who want better control over everyday money movement instead of juggling separate tools.

10

Stashfin

Stashfin is more credit-focused than banking-focused. It offers a digital line-of-credit card with flexible access to funds, digital approval, and repayment options that appeal to users needing quick credit.

Best for:

Users with flexible credit needs

People who prefer revolving credit

Users looking to build or rebuild credit

Key features:

Digital line-of-credit card

Quick approval and disbursal

Cashback, ATM withdrawals, and EMI options

Why choose it:

Stashfin is useful if your main priority is flexible borrowing rather than a full-service banking setup.

11

Chqbook

Chqbook is built for small Indian business owners like kirana stores, local merchants, and proprietors. Its multilingual and mobile-first approach makes it more accessible for regional users.

Best for:

Kirana stores and local merchants

Small proprietors and neighbourhood businesses

Users who prefer vernacular interfaces

Key features:

Zero-balance digital current account

Multilingual app support

Basic banking tools plus access to loans and insurance

Why choose it:

Chqbook feels more rooted in the needs of small Indian businesses than many startup-focused fintech platforms.

12

ZikZuk

ZikZuk, from the Zaggle group, focuses on financial visibility for SMEs. It combines a business credit card with dashboards that help founders track receivables, payables, and cash flow.

Best for:

SME founders with multiple accounts

Businesses wanting better cash-flow visibility

Founders who need a credit card plus finance dashboard

Key features:

Business credit card for founders

Finance dashboards and forecasting tools

Multi-bank account aggregation

Why choose it:

ZikZuk is useful if your main challenge is not just banking, but getting a clearer picture of your business finances in one place.

13

Finin

Finin was one of the early consumer neobanks in India and helped popularize app-first saving and goal-based money management. It has since become part of Open Financial Technologies.

Best for:

Users looking for easy onboarding and high security

People who need AI Powered Insights for their money

Key features:

Goal-based saving experience

Consumer-friendly digital banking design

Now supports Open’s broader banking infrastructure

Why choose it:

Choose it for its rapid, paperless onboarding, high-interest savings via partner SBM Bank, and smart spending analytics to achieve financial independence.

14

Zolve

Zolve focuses on Indians moving to the US or Canada. It helps students and professionals set up accounts and begin building credit before they arrive abroad.

Best for:

Indian students moving abroad

Professionals relocating to the US or Canada

Users who want banking ready before landing

Key features:

Cross-border account setup support

Credit cards without prior local credit history

Online application using Indian passport and visa details

Why choose it:

Zolve solves a real relocation problem by helping users start banking and credit-building early, which makes settling abroad much easier.

1

Freo

Freo stands out as one of the most well-rounded neobanking apps in India because it combines saving, credit, and everyday money management in one place. Instead of using separate apps for borrowing, tracking expenses, and managing payments, you get a more connected experience here.

Best for:

Users who want savings and flexible credit in one app

Salaried millennials and young professionals

People looking for a practical alternative to traditional banking apps

Key features:

Digital savings and deposit products through partner banks

Personal credit line, cards, EMI options, and BNPL access

Expense tracking and money management tools

Fixed deposits with an impressive 9.1% return rate.

Why choose it:

Freo works well if you want one app that supports both daily spending and credit needs without feeling scattered.

2

Fi Money

Fi Money is a polished consumer neobank that offers a zero-balance digital savings and salary account through Federal Bank. Its clean app, rewards, and goal-based saving tools make it appealing to users who want banking to feel modern and easy to use.

Best for:

Salaried professionals

Users who like cashback and rewards

People who want a zero-balance digital account with UPI

Key features:

Zero-balance savings and salary account

Fi Jars for goal-based saving

Cashback, rewards, and app-based controls

Why choose it:

Fi is a strong option if you want a salary account with useful saving tools, spending insights, and a more engaging app experience.

3

Jupiter

Jupiter is popular for keeping digital banking simple. It offers a zero-balance savings account with Federal Bank and focuses on clean design, smooth onboarding, and helpful budgeting tools for everyday users.

Best for:

First-time neobank users

Young professionals who want spending insights

Users looking for a simple zero-balance account

Key features:

Zero-balance savings account

Instant onboarding with UPI access

Budgeting, expense tracking, and saving pots

Why choose it:

Jupiter is a good fit if you want a clean, no-fuss app that helps you understand spending and manage savings better.

4

Niyo

Niyo is best known for travel-focused banking. It offers accounts and cards through partner banks and is especially useful for people who spend abroad and want to avoid high forex charges.

Best for:

Frequent international travellers

Students going abroad

Users who want lower forex costs

Key features:

Zero forex markup on select transactions

Travel-friendly account and card options

App controls for card use and tracking

Why choose it:

If overseas spending is a big part of your life, Niyo can help you save on forex fees and manage travel spending more smoothly.

5

RazorpayX

RazorpayX is built for startups and SMEs, not retail users. It helps businesses manage current accounts, payouts, payroll, taxes, and collections through one connected finance platform.

Best for:

Startups and digital businesses

Finance teams handling payouts and taxes

Businesses already using Razorpay services

Key features:

Digital current accounts

Automated payouts and collections

Tax payments and integrations with tools like Tally and Zoho

Why choose it:

RazorpayX is ideal if your business wants faster finance operations and less manual work across banking and payments.

6

InstantPay

InstantPay is a business-focused neobank designed for SMEs that want quick digital onboarding and easy access to current account and cash-management tools without traditional banking friction.

Best for:

Small and medium businesses

Firms with mobile-first teams

Businesses seeking simple digital current accounts

Key features:

Digital current accounts and cash-management tools

Collections, payouts, and reconciliation

Mobile and web access with multi-bank support

Why choose it:

InstantPay makes sense for businesses that want practical digital banking tools without moving into a more complex enterprise system.

7

FamPay

FamPay targets teenagers and families by offering supervised digital payments. It helps teens use UPI and cards while parents stay involved through funding and controls.

Best for:

Parents introducing kids to digital money

Teenagers making online and offline payments

Families building financial literacy early

Key features:

Teen-focused accounts with parental controls

Numberless card for added safety

UPI payments and spend tracking

Why choose it:

FamPay balances independence and supervision well, making it one of the more established options in India’s teen neobank segment.

8

Mahila Money

Mahila Money focuses on women, especially women entrepreneurs and first-time borrowers. Rather than offering generic fintech products, it tries to address real financial gaps faced by women-led businesses.

Best for:

Women micro-entrepreneurs

Home-based business owners

First-time women borrowers

Key features:

Savings, loans, and insurance through partners

Digital onboarding tailored to women-led ventures

Financial guidance and educational content

Why choose it:

Mahila Money stands out because it is built around financial inclusion and offers a more focused experience than mainstream banking apps.

9

Open Money

Open Money is one of the biggest SME neobanking platforms in India. It combines current accounts, invoicing, payouts, expense management, and business credit in one system.

Best for:

SMEs and startups

Founders who want more than a basic current account

Businesses looking for banking and invoicing together

Key features:

Business current accounts and expense tools

Integrated invoicing and payments

Credit access through partnerships

Why choose it:

Open is a great choice for business owners who want better control over everyday money movement instead of juggling separate tools.

10

Stashfin

Stashfin is more credit-focused than banking-focused. It offers a digital line-of-credit card with flexible access to funds, digital approval, and repayment options that appeal to users needing quick credit.

Best for:

Users with flexible credit needs

People who prefer revolving credit

Users looking to build or rebuild credit

Key features:

Digital line-of-credit card

Quick approval and disbursal

Cashback, ATM withdrawals, and EMI options

Why choose it:

Stashfin is useful if your main priority is flexible borrowing rather than a full-service banking setup.

11

Chqbook

Chqbook is built for small Indian business owners like kirana stores, local merchants, and proprietors. Its multilingual and mobile-first approach makes it more accessible for regional users.

Best for:

Kirana stores and local merchants

Small proprietors and neighbourhood businesses

Users who prefer vernacular interfaces

Key features:

Zero-balance digital current account

Multilingual app support

Basic banking tools plus access to loans and insurance

Why choose it:

Chqbook feels more rooted in the needs of small Indian businesses than many startup-focused fintech platforms.

12

ZikZuk

ZikZuk, from the Zaggle group, focuses on financial visibility for SMEs. It combines a business credit card with dashboards that help founders track receivables, payables, and cash flow.

Best for:

SME founders with multiple accounts

Businesses wanting better cash-flow visibility

Founders who need a credit card plus finance dashboard

Key features:

Business credit card for founders

Finance dashboards and forecasting tools

Multi-bank account aggregation

Why choose it:

ZikZuk is useful if your main challenge is not just banking, but getting a clearer picture of your business finances in one place.

13

Finin

Finin was one of the early consumer neobanks in India and helped popularize app-first saving and goal-based money management. It has since become part of Open Financial Technologies.

Best for:

Users looking for easy onboarding and high security

People who need AI Powered Insights for their money

Key features:

Goal-based saving experience

Consumer-friendly digital banking design

Now supports Open’s broader banking infrastructure

Why choose it:

Choose it for its rapid, paperless onboarding, high-interest savings via partner SBM Bank, and smart spending analytics to achieve financial independence.

14

Zolve

Zolve focuses on Indians moving to the US or Canada. It helps students and professionals set up accounts and begin building credit before they arrive abroad.

Best for:

Indian students moving abroad

Professionals relocating to the US or Canada

Users who want banking ready before landing

Key features:

Cross-border account setup support

Credit cards without prior local credit history

Online application using Indian passport and visa details

Why choose it:

Zolve solves a real relocation problem by helping users start banking and credit-building early, which makes settling abroad much easier.

1

Freo

Freo stands out as one of the most well-rounded neobanking apps in India because it combines saving, credit, and everyday money management in one place. Instead of using separate apps for borrowing, tracking expenses, and managing payments, you get a more connected experience here.

Best for:

Users who want savings and flexible credit in one app

Salaried millennials and young professionals

People looking for a practical alternative to traditional banking apps

Key features:

Digital savings and deposit products through partner banks

Personal credit line, cards, EMI options, and BNPL access

Expense tracking and money management tools

Fixed deposits with an impressive 9.1% return rate.

Why choose it:

Freo works well if you want one app that supports both daily spending and credit needs without feeling scattered.

2

Fi Money

Fi Money is a polished consumer neobank that offers a zero-balance digital savings and salary account through Federal Bank. Its clean app, rewards, and goal-based saving tools make it appealing to users who want banking to feel modern and easy to use.

Best for:

Salaried professionals

Users who like cashback and rewards

People who want a zero-balance digital account with UPI

Key features:

Zero-balance savings and salary account

Fi Jars for goal-based saving

Cashback, rewards, and app-based controls

Why choose it:

Fi is a strong option if you want a salary account with useful saving tools, spending insights, and a more engaging app experience.

3

Jupiter

Jupiter is popular for keeping digital banking simple. It offers a zero-balance savings account with Federal Bank and focuses on clean design, smooth onboarding, and helpful budgeting tools for everyday users.

Best for:

First-time neobank users

Young professionals who want spending insights

Users looking for a simple zero-balance account

Key features:

Zero-balance savings account

Instant onboarding with UPI access

Budgeting, expense tracking, and saving pots

Why choose it:

Jupiter is a good fit if you want a clean, no-fuss app that helps you understand spending and manage savings better.

4

Niyo

Niyo is best known for travel-focused banking. It offers accounts and cards through partner banks and is especially useful for people who spend abroad and want to avoid high forex charges.

Best for:

Frequent international travellers

Students going abroad

Users who want lower forex costs

Key features:

Zero forex markup on select transactions

Travel-friendly account and card options

App controls for card use and tracking

Why choose it:

If overseas spending is a big part of your life, Niyo can help you save on forex fees and manage travel spending more smoothly.

5

RazorpayX

RazorpayX is built for startups and SMEs, not retail users. It helps businesses manage current accounts, payouts, payroll, taxes, and collections through one connected finance platform.

Best for:

Startups and digital businesses

Finance teams handling payouts and taxes

Businesses already using Razorpay services

Key features:

Digital current accounts

Automated payouts and collections

Tax payments and integrations with tools like Tally and Zoho

Why choose it:

RazorpayX is ideal if your business wants faster finance operations and less manual work across banking and payments.

6

InstantPay

InstantPay is a business-focused neobank designed for SMEs that want quick digital onboarding and easy access to current account and cash-management tools without traditional banking friction.

Best for:

Small and medium businesses

Firms with mobile-first teams

Businesses seeking simple digital current accounts

Key features:

Digital current accounts and cash-management tools

Collections, payouts, and reconciliation

Mobile and web access with multi-bank support

Why choose it:

InstantPay makes sense for businesses that want practical digital banking tools without moving into a more complex enterprise system.

7

FamPay

FamPay targets teenagers and families by offering supervised digital payments. It helps teens use UPI and cards while parents stay involved through funding and controls.

Best for:

Parents introducing kids to digital money

Teenagers making online and offline payments

Families building financial literacy early

Key features:

Teen-focused accounts with parental controls

Numberless card for added safety

UPI payments and spend tracking

Why choose it:

FamPay balances independence and supervision well, making it one of the more established options in India’s teen neobank segment.

8

Mahila Money

Mahila Money focuses on women, especially women entrepreneurs and first-time borrowers. Rather than offering generic fintech products, it tries to address real financial gaps faced by women-led businesses.

Best for:

Women micro-entrepreneurs

Home-based business owners

First-time women borrowers

Key features:

Savings, loans, and insurance through partners

Digital onboarding tailored to women-led ventures

Financial guidance and educational content

Why choose it:

Mahila Money stands out because it is built around financial inclusion and offers a more focused experience than mainstream banking apps.

9

Open Money

Open Money is one of the biggest SME neobanking platforms in India. It combines current accounts, invoicing, payouts, expense management, and business credit in one system.

Best for:

SMEs and startups

Founders who want more than a basic current account

Businesses looking for banking and invoicing together

Key features:

Business current accounts and expense tools

Integrated invoicing and payments

Credit access through partnerships

Why choose it:

Open is a great choice for business owners who want better control over everyday money movement instead of juggling separate tools.

10

Stashfin

Stashfin is more credit-focused than banking-focused. It offers a digital line-of-credit card with flexible access to funds, digital approval, and repayment options that appeal to users needing quick credit.

Best for:

Users with flexible credit needs

People who prefer revolving credit

Users looking to build or rebuild credit

Key features:

Digital line-of-credit card

Quick approval and disbursal

Cashback, ATM withdrawals, and EMI options

Why choose it:

Stashfin is useful if your main priority is flexible borrowing rather than a full-service banking setup.

11

Chqbook

Chqbook is built for small Indian business owners like kirana stores, local merchants, and proprietors. Its multilingual and mobile-first approach makes it more accessible for regional users.

Best for:

Kirana stores and local merchants

Small proprietors and neighbourhood businesses

Users who prefer vernacular interfaces

Key features:

Zero-balance digital current account

Multilingual app support

Basic banking tools plus access to loans and insurance

Why choose it:

Chqbook feels more rooted in the needs of small Indian businesses than many startup-focused fintech platforms.

12

ZikZuk

ZikZuk, from the Zaggle group, focuses on financial visibility for SMEs. It combines a business credit card with dashboards that help founders track receivables, payables, and cash flow.

Best for:

SME founders with multiple accounts

Businesses wanting better cash-flow visibility

Founders who need a credit card plus finance dashboard

Key features:

Business credit card for founders

Finance dashboards and forecasting tools

Multi-bank account aggregation

Why choose it:

ZikZuk is useful if your main challenge is not just banking, but getting a clearer picture of your business finances in one place.

13

Finin

Finin was one of the early consumer neobanks in India and helped popularize app-first saving and goal-based money management. It has since become part of Open Financial Technologies.

Best for:

Users looking for easy onboarding and high security

People who need AI Powered Insights for their money

Key features:

Goal-based saving experience

Consumer-friendly digital banking design

Now supports Open’s broader banking infrastructure

Why choose it:

Choose it for its rapid, paperless onboarding, high-interest savings via partner SBM Bank, and smart spending analytics to achieve financial independence.

14

Zolve

Zolve focuses on Indians moving to the US or Canada. It helps students and professionals set up accounts and begin building credit before they arrive abroad.

Best for:

Indian students moving abroad

Professionals relocating to the US or Canada

Users who want banking ready before landing

Key features:

Cross-border account setup support

Credit cards without prior local credit history

Online application using Indian passport and visa details

Why choose it:

Zolve solves a real relocation problem by helping users start banking and credit-building early, which makes settling abroad much easier.

How Do Neobanks Work?

Even though neobanks feel very different from traditional banks, the core idea remains the same. They still provide financial services such as accounts, payments, and cards. The difference lies in how those services are delivered. Here are the main elements that power neobanks.

To understand neobanks, think of them as the "Netflix of Banking"—they replaced the "Blockbuster" (physical branches) with a seamless digital app.

1

1

Digital-First Approach

Neobanks are built around apps and web platforms instead of physical branches. The entire banking experience happens online.

You can open an account, transfer money, check balances, freeze cards, or review spending without visiting an office. Everything is designed to work smoothly on a smartphone or laptop.

This approach also allows neobanks to launch updates and improvements much faster than traditional banks.

2

2

Integration with Traditional Banks

In India and many other countries, most neobanks do not hold full banking licenses. Instead, they collaborate with licensed banks that handle regulatory responsibilities and hold customer deposits.

The neobank focuses on the user experience, while the partner bank provides the regulated banking infrastructure.

This partnership model allows neobanks to offer legitimate banking services without building a full banking institution from scratch.

3

3

Technology-Driven Services

Technology plays a central role in how neobanks operate. Their platforms are built to analyse spending patterns, track transactions instantly, and provide useful financial insights.

For example, many apps automatically group your spending into categories such as food, travel, or shopping. This helps users understand where their money is going without manually tracking expenses.

These insights often turn everyday banking into something more interactive and informative.

4

4

Customer Onboarding

Opening an account with a neobank is usually quick. Most platforms rely on digital identity verification.

Users upload documents, complete a verification process, and receive account access within minutes. In many cases, there is no need to sign physical paperwork or visit a branch.

This fast onboarding process is one of the biggest reasons people try neobanks.

5

5

Innovative Features

Neobanks often experiment with features that traditional banks take longer to introduce.

Some platforms offer automatic savings tools, spending limits, smart budgeting options, or virtual debit cards for safer online payments.

For businesses, neobanks may include tools such as payment collection links, expense dashboards, or automated bookkeeping integrations.

These features are designed to make everyday money management easier.

6

6

Enhanced Security

Although neobanks operate online, security remains a major priority.

Most platforms include multiple layers of protection such as biometric login, instant transaction alerts, card controls, and two-factor authentication.

Users can also block or freeze cards instantly through the app if they notice suspicious activity.

Because everything is digital, monitoring and responding to unusual transactions can often happen much faster.

How to Choose the Right Neobank?

Not every neobank is built for the same purpose. Some focus on personal banking, while others target startups, freelancers, or small businesses.

Before opening an account, it helps to review a few basic factors.

First, check which bank supports the neobank platform. Since deposits are technically held with the partner bank, its reliability matters.

Next, look closely at the app experience. Since the entire service runs digitally, the interface should be simple, stable, and easy to navigate.

You should also review features such as transaction limits, card benefits, and expense tracking tools. Some apps are designed mainly for payments, while others focus on budgeting or financial planning.

Finally, check the fee structure. Many neobanks promote zero-balance accounts, but certain services may still carry charges.

Neobanks vs Traditional Banks

| Feature | Neobanks | Traditional Banks |

|---|---|---|

| Physical Presence | Operate entirely online | Maintain branch networks |

| Account Setup | Quick digital registration | Often requires more formal steps |

| Infrastructure | Work with licensed banking partners | Hold their own banking licenses |

| Fees | Often lower due to digital operations | May include maintenance or service charges |

| Financial Tools | Built-in budgeting and analytics | Limited insights in most apps |

| Customer Access | Mobile and web apps | Branch, phone, and digital access |

| Service Updates | Faster feature rollouts | Slower changes due to legacy systems |

Closing Thoughts

Neobanks are not trying to replace traditional banks completely. Instead, they offer a different way to manage everyday finances.

By combining digital platforms with licensed banking partners, they bring speed, flexibility, and modern tools into routine financial activities.

For people who prefer managing money through apps and want more visibility into their spending habits, neobanks can be a convenient option.

FAQs

Are neobank accounts free?

Many neobanks provide accounts that do not require a minimum balance. However, some services such as premium cards or advanced features may include small fees.

Which neobanks are popular in India right now?

Are neobanks regulated in India?

What makes neobanks different from traditional banks?

What services do neobanks provide?

Are neobanks useful for businesses?

Can I open an account quickly with a neobank?

Do neobanks support UPI payments?

Do neobanks offer loans?

Do neobanks issue debit cards?

Do I need to visit a branch to open an account?

Do neobanks charge maintenance fees?

Enjoy the perks that Freo brings you. Earn up to 9.1% interest on FD and Invest in Digital Gold with Freo now!

Enjoy the perks that Freo brings you. Earn up to 9.1% interest on FD and Invest in Digital Gold with Freo now!

Enjoy the perks that Freo brings you. Earn up to 9.1% interest on FD and Invest in Digital Gold with Freo now!

Make the Move

What are you waiting for?

Our Products

Quick Links

MWYN Tech Private Limited

CIN: U72200KA2015PTC083534

Address: G-405,4th Floor - Gamma Block, Sigma Soft Tech Park Varthur, Kodi Whitefield Post, Bangalore - 560066

Copyright © 2026 MWYN Tech Pvt Ltd. All rights reserved.

Make the Move

What are you waiting for?

Our Products

Quick Links

Calculators

MWYN Tech Private Limited

CIN: U72200KA2015PTC083534

Address: G-405,4th Floor - Gamma Block, Sigma Soft Tech Park Varthur, Kodi Whitefield Post, Bangalore - 560066

Copyright © 2026 MWYN Tech Pvt Ltd. All rights reserved.

Make the Move

What are you waiting for?

Our Products

Quick Links

MWYN Tech Private Limited

CIN: U72200KA2015PTC083534

Address: G-405,4th Floor - Gamma Block, Sigma Soft Tech Park Varthur, Kodi Whitefield Post, Bangalore - 560066

Copyright © 2026 MWYN Tech Pvt Ltd. All rights reserved.